SME Graduation: The Next Frontier of Bangladesh’s Economic Transformation

Commercial banks can play a decisive role in turning small enterprises into competitive engines of growth.

Small and Medium Enterprises (SMEs) are widely regarded as the backbone of modern economies. In Bangladesh, the SME sector contributes significantly to employment generation, value addition, and regional economic development. As the country aspires to achieve upper-middle-income status, strengthening SME entrepreneurship and enabling their gradual graduation into larger, more productive enterprises has become a national priority.

In this transformation process, commercial banks have a pivotal role to play. Beyond traditional lending, banks can act as catalysts for entrepreneurship development, financial inclusion, and sustainable economic growth.

SMEs in the Bangladesh Economy

SMEs constitute the overwhelming majority of business enterprises in Bangladesh and provide employment for millions of people across both urban and rural areas. They contribute significantly to manufacturing output, trade, and service sector activities.

The government and regulators such as Bangladesh Bank have emphasized SME development through policy incentives, refinance schemes, and credit targets for banks. However, the challenge remains not only to support SME creation but also to help them graduate into stronger, formal and competitive enterprises.

The diagram should be:

SME Graduation =Entrepreneurship + Finance + Technology + Market Access + Governance

Challenges Faced by SME Entrepreneurs

Despite their importance, SME entrepreneurs face several structural challenges such as:

• limited access to formal finance;

• inadequate managerial and financial skills;

• weak market linkages;

• lack of collateral;

• technological gaps

• entrepreneurship development training;

• export supports

Many small businesses remain trapped in the informal sector and fail to scale up due to these constraints. Addressing these issues requires a more proactive engagement from the banking sector.

How Commercial Banks Can Promote SME Entrepreneurship!!

Commercial banks can contribute to SME entrepreneurship development in several strategic ways.

1. Expanding Access to Finance:

Access to credit remains one of the most critical barriers for SMEs. Banks should design specialized SME loan products with simplified procedures, flexible collateral requirements, and risk-based pricing. Credit scoring models and alternative data analysis can help banks lend to promising entrepreneurs who lack traditional collateral.

2. Supporting Entrepreneurial Capacity Building:

Banks can collaborate with training institutions, chambers of commerce, and development agencies to provide financial literacy and business management training for SME clients. Educating entrepreneurs on accounting practices, cash flow management, and digital transactions significantly improves business sustainability. Some of banks already involved but many of them reluctant.

3. Facilitating SME Graduation:

A key objective of SME policy is enabling businesses to graduate from micro and small enterprises into medium and eventually larger firms. Banks can support this transition by offering:

• step-up financing based on business growth;

• working capital facilities;

• trade finance services;

• investment loans for technology upgrades.

A structured “graduation financing pathway” can help successful SMEs scale their operations gradually.

4. Strengthening Digital and Financial Infrastructure:

Digital banking solutions can significantly improve SME access to finance. Mobile banking, digital payment systems, and online loan processing reduce transaction costs and expand financial inclusion.

Bangladesh has already made significant progress in digital finance, and banks can leverage these platforms to reach entrepreneurs in rural and semi-urban regions.

5. Promoting Women Entrepreneurship:

Women entrepreneurs remain underrepresented in formal business sectors. Targeted SME credit programs, advisory services, and mentorship initiatives can empower more women to establish and grow businesses. Such initiatives not only promote gender equality but also expand the country’s entrepreneurial base.

6. Integrating SMEs into Value Chains:

Commercial banks can play an important role in linking SMEs with larger corporations through supply-chain financing and invoice discounting. These financial instruments help SMEs maintain liquidity and expand market opportunities.

7. Integration with MFIs:

Micro Financial Institutions (MFIs) are working with micro finance in rural level. They are creating promoters of micro finance; some of them are doing well and graduating from micro to small enterprise. If commercial banks have a wing to work with MFIs, they can get those graduation processes and further develop them to medium enterprises, then to large.

8. Policy Support and Regulatory Role:

The central bank, Bangladesh Bank, has introduced several initiatives to encourage SME lending, including refinance schemes and sector-specific credit targets. But this is not sufficient. Government should have integrating committee at district level, They will monitor the effectiveness support from commercial banks and Bangladesh Bank.

Continued policy support, combined with stronger risk management frameworks, can further encourage banks to expand SME financing.

9. Towards Sustainable SME Development:

For Bangladesh to sustain long-term economic growth, SMEs must evolve from small survival enterprises into dynamic and competitive businesses capable of generating employment, exports, and innovation.

Commercial banks are uniquely positioned to facilitate this transformation. By combining financing with advisory support, technological integration, and inclusive banking practices, they can help build a vibrant entrepreneurial ecosystem. Bangladesh Bank and SME Foundation should judge the effectiveness.

10. Towards Large Capital Drawing From Capital Market:

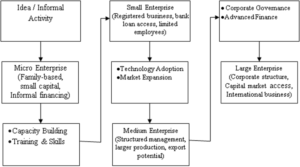

The Graduation process of Micro Enterprise to Medium Enterprise to Large Corporate are being made from MFIs to Commercial Banks to Capital Markets for financing. During this journey of entrepreneurs, they should be supported by all the related institutions and finally they should be booked in SME board of Bangladesh Capital Market for their funding, establishing corporate Governance and should be transparent & accountable to the society.

Continues graduation process from Micro Enterprise to Medium Enterprise to Large Corporate can be shown in the diagram as:

Conclusion:

SME entrepreneurship development and graduation are essential for Bangladesh’s next stage of economic transformation. Commercial banks must move beyond traditional lending roles and become strategic partners in enterprise growth.

If the financial sector, policymakers, and entrepreneurs work together, SMEs can emerge as powerful engines of inclusive and sustainable economic development in Bangladesh.

Writer: Mohammed Shahid Ullah FCA,

A Senior Banker.

Can reach at: rafan3379@gmail.com

The Indispensability of the SME Sector for Bangladesh’s Development:

In the context of a developing nation like Bangladesh, the Small and Medium Enterprise (SME) sector is not just a component of the economy—it is its very heartbeat. Often referred to as the “engine of growth,” the SME sector plays a pivotal role in poverty alleviation, employment generation, and industrialization. It is no exaggeration to say that the holistic development of Bangladesh is impossible if the SME sector is left behind.

1. The Largest Source of Employment.

2. Poverty Alleviation and Rural Development.

3. Contribution to GDP and Export Diversity.

4. Innovation and Industrial Linkage.

Challenges to Overcome:

a) Access to Finance: Difficulty in obtaining low-interest bank loans.

b) Infrastructure: Inadequate power supply and poor transportation in rural areas.

c) Technical Skill Gap: A lack of modern technology and vocational training.

To achieve the goal of becoming a “Developed Bangladesh” by 2041, the government and financial institutions must prioritize the SME sector. By providing easier access to credit, improving infrastructure, and offering policy support, Bangladesh can ensure an inclusive and resilient economy. Simply put, the dream of a “Sonar Bangla” (Golden Bengal) cannot be realized without a thriving SME sector.

Thanks

sir

Bankers should work for the creation of entrepreneurs and graduate them….